UPDATED: Why Credit Suisse "nearly" went bankrupt and whether it has a chance to survive

The central bank bailout should be enough to compensate for depositors' panic

On 14 March, following a series of bank failures in the United States, Swiss Credit Suisse announced that its auditor PwC had found "significant weaknesses" in the bank's financial reporting controls. The bank postponed the release of its audited annual report after the US Securities and Exchange Commission requested additional information about the issues.

As early as Wednesday, 15 March, after the share price fell by 31%, the bank asked the Swiss National Bank to publicly support it. The total amount of support is CHF 50 billion.

However, the bailout was only one element in the plan to save the financial giant, as discussions were underway to take it over by more stable market participants. The saga ended on 19 March, when it was announced that UBS was buying the largest bank in Switzerland.

Five months ago, Mind published an article titled "Swiss bank Credit Suisse is predicted to fail and compared to Lehman Brothers. Why is this incorrect?".

In it, we analysed the situation around Credit Suisse in detail.

Mind offers a look at what has changed since the review and whether the outcome of the story can be considered a bankruptcy.

Reviewing and updating our opinions

In our October analysis, we focused on the bank's balance sheet and financial results, so let's start with them. Since then, the bank has published its Q3 2022 report (we advised you to pay attention to this event on 27 October), as well as its annual reporton 9 February. The bank's shares (SWX: CSGN) reacted to both publications with serious declines: -20% and -16%, respectively.

Let's focus on the annual report. Despite the fact that it talked about certain successes in the bank's strategic reform, investors were primarily interested in the results here and now, and they were disappointing.

The net loss for the year reached CHF 7.3 billion. At the time of our October publication, only CHF 1.6 billion of losses were known for the first half of the year, and analysts' forecasts were that this amount would double by the end of the year. As you can see, the situation turned out to be much worse.

We compared the loss to the bank's capital and pointed out that it was the capital that would be the ultimate source of covering these losses. After that, the bank managed to raise CHF 4 billion in additional capital, which allowed it to maintain its capital at CHF 45 billion.

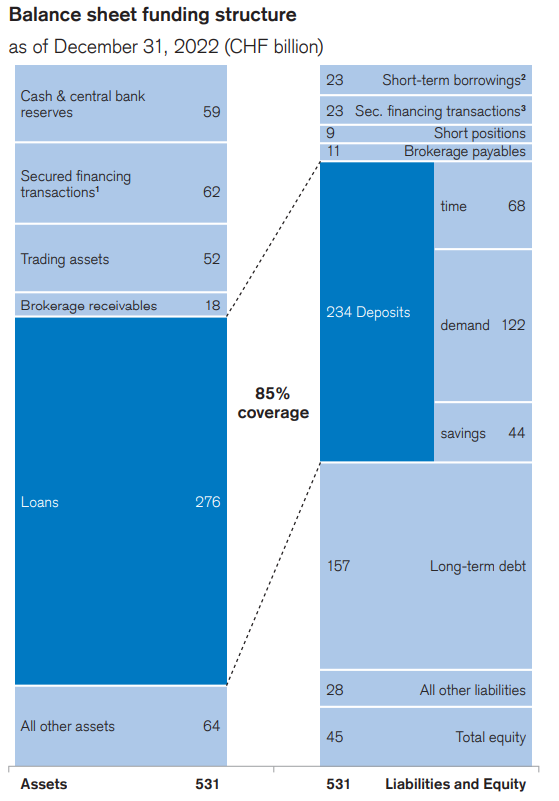

At the same time, the bank's total assets declined sharply in the last quarter of the year to CHF 531 billion (CHF 756 billion at the end of 2021, CHF 700 billion at the end of Q3 2022).

There was a massive outflow of deposits (especially in October, at the peak of scepticism), and net income was down 34% compared to 2021. Deposit coverage of loans fell from 129% to 85%.

We provided a comparison of the bank's assets and liabilities, and now we are publishing the updated data.

Source: Annual Report, p. 111

Changes in relative indicators

The share of capital in the bank's assets increased to 8.5% (from 6.3% in the first half of 2022).

The CET1 ratio (Common Equity Tier 1 ratio) also increased to 14.1% (13.5%).

However, the net stable funding ratio (NSFR) decreased. The available funding covers the potential need for it by 117% (CHF 343.2 billion vs CHF 292.5 billion), while six months ago it was a more solid 132%. For more details on these figures, see our October review.

Of course, the reform programmes announced at the end of the year could not have shown their effect so quickly. Operating expenses are still high, and the processes of liquidating some assets and changing the group's business structure have only just begun. Thus, part of the assets was allocated to a separate segment for the sale of the Capital Release Unit:

The bank's report says it expects losses in 2023. In fact, investors are offered to invest strategically, relying on the success of reforms. And this can be a profitable bet in a stable external environment. However, the US "bank bust" has changed the situation, and it is financial institutions with weak businesses that may be hit hardest.

What is happening now?

We now know that Credit Suisse has agreed to access CHF 50 billion in funding from the Swiss Central Bank. How significant is this amount? To answer this question, we need to delve into the structure of assets and liabilities in terms of maturity. As we wrote in the SVB review, most problems materialise when liabilities need to be repaid quickly, while assets are placed "long term".

Source: Annual Report 2022, p. 114

We focus on the first three groups:

- Current (on demand).

- Less than 1 month.

- Between 1 and 3 months.

We see an excess of current liabilities by 36 billion, while in the other two groups, on the contrary, assets cover liabilities by a difference of 32 billion. The announced 50 billion from the central bank mathematically covers the difference in the first group. As a rule, in such cases, it is not necessary to use the entire amount, but rather to make it available when needed.

Special attention should be paid to the category "Trading assets, at fair value" for CHF 65 billion. The word "fair" here refers to the market value of the assets, unlike the situation with SVB, where the lion's share of securities were valued at book value and did not take into account price declines.

We are aware that such a comparison does not detail the quality and actual performance of each of these asset groups, as we can only rely on publicly available data. Asset quality may deteriorate in line with general economic trends and this may be reflected in the future and is difficult to predict.

However, the comparison of absolute amounts today allows us to model extreme scenarios such as a complete withdrawal of all current customer deposits (CHF 167 billion). The reserve of CHF 50 billion seems to be a reliable cushion for the bank's continued operation.

Mind will continue to monitor the situation with Switzerland's second-largest bank by assets and analyse developments. At this point, the key dates will be: 4 April, when the general meeting of shareholders is scheduled to take place, and 27 April, when the report for the Q1 of 2023 will be published.

If you have read this article to the end, we hope that means it was useful for you.

We work to ensure that our journalistic and analytical work is of high quality, and we strive to perform it as competently as possible. This also requires financial independence. Support us for only UAH 196 per month.

Become a Mind subscriber for just USD 5 per month and support the development of independent business journalism!

You can unsubscribe at any time in your LIQPAY account or by sending us an email: [email protected]